AML regulations are designed to safeguard the integrity of financial institutions (FIs) in a fast-paced, evolving landscape—a robust anti-money laundering compliance program can’t be overstated. By following regulations, FIs can protect themselves from becoming unwitting accomplices to illicit activities. While firms implement stringent AML measures, the onus of ensuring compliance often falls on the shoulders of senior management. In the event of compliance failures, these leaders may find themselves facing not only professional repercussions but also personal liability. Compliance cannot be achieved without a strong ethical culture led by senior management who play a pivotal role in defining, shaping, and fostering this culture. In this role, senior management would be the driving force behind ethical behavior, regulatory adherence, and overall corporate integrity.

Rising Regulatory Scrutiny

Lately, regulatory scrutiny across the globe in AML compliance has been on the rise. FIs are required to have more robust systems in place to detect and prevent money laundering activities. Regulators are not just looking at the systems in place—they’re determining if these systems are being implemented effectively. Regulators are increasingly holding institutions accountable for lapses in their AML compliance programs, and there is a shift from institution to individual accountability. Executives and senior management are now under the lens and are expected to take ownership of their institution’s AML compliance program. The aim of the regulators is to ensure that those in positions of authority cannot evade responsibility by hiding behind the corporate veil.

The FATF also emphasizes the importance of senior management involvement and oversight in AML compliance, stating that “senior management should be fully committed to, and actively involved in, ensuring that the FI maintains an effective AML/CFT program” and that “senior management should be informed of compliance failures and significant AML/CFT risks”.

Our analysis of recent enforcement actions due to breach in AML/Sanctions compliance has revealed that some FIs lack compliance culture and, in some cases, senior management commitment towards regulations.

Navigating the Terrain of Compliance Culture

Establishing and maintaining a culture of compliance comes with challenges. The key obstacles faced by senior management when undertaking the formidable task of fostering a culture that prioritizes adherence to laws, regulations, and ethical standards are:

- Resistance to Change: One of the primary hurdles faced by senior management is the inherent resistance to change within the institution. Employees may be accustomed to existing practices and often view changes to compliance measures as disruptive. Overcoming this resistance requires effective communication and a clear articulation of the benefits of compliance for both the FI and its individuals.

- Dynamic Regulatory Environment: The ever-evolving regulatory landscape poses a continual challenge. Senior management needs to stay abreast of changes in laws and industry regulations and adapt compliance measures accordingly. This requires a proactive approach to compliance management and a commitment to ongoing regulatory education.

- Inconsistent Enforcement: Consistency in enforcing compliance standards is critical for building trust and credibility. Inconsistencies can lead to confusion and undermine the entire compliance framework. Senior management must ensure that policies are uniformly applied across the institution, and deviations are addressed promptly and fairly.

- Technological Challenges: The integration of technology into compliance processes introduces its own set of challenges. Senior management must grapple with selecting and implementing appropriate technologies, ensuring they align with organizational needs, and providing adequate training to employees to use these tools effectively.

- Cultural and Linguistic Differences: In the context of globalized FIs, differing cultures and languages can impede the uniform adoption of compliance standards. Senior management must navigate these differences by tailoring communication and initiatives to resonate with diverse cultural backgrounds, fostering a sense of unity in compliance goals.

- Employee Engagement: Establishing a culture of compliance hinges on active participation and engagement from all levels. Senior management should create opportunities for employees to be involved in the compliance process, encouraging a sense of ownership and responsibility towards maintaining ethical standards.

- Balancing Short-Term Goals and Long-Term Commitments: Pressures to meet short-term objectives may sometimes overshadow the importance of long-term compliance. Striking a balance between immediate goals and sustaining a commitment to compliance requires strategic decision-making and a focus on the FI’s enduring success.

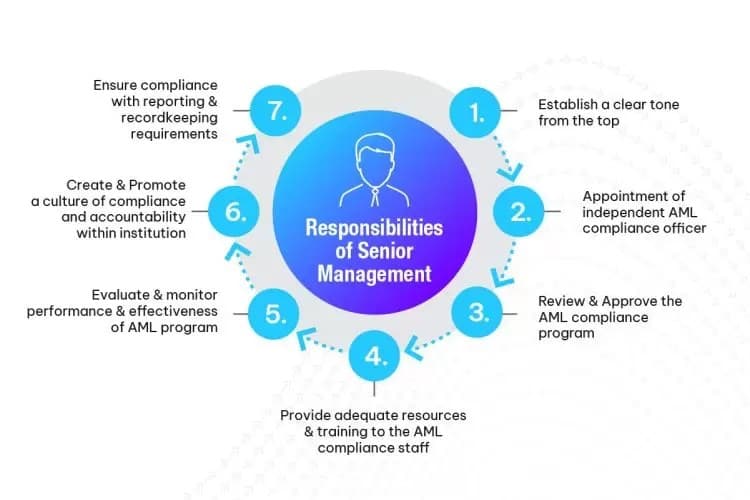

Responsibilities to Improve Compliance Culture

Some of the key actions board members or senior management can take to improve compliance culture:

- Establish a clear tone from the top that AML compliance is a strategic priority and a core value of the institution. This can be done by communicating regularly and openly with the staff, customers, and stakeholders about the importance and benefits of AML compliance, and by setting an example of ethical and compliant behavior.

- Appointment of an independent AML compliance officer who has the necessary skills, experience, and authority to oversee and manage the AML compliance program. The AML compliance officer should report directly to the management body or a senior executive and should have sufficient resources and support to perform their duties effectively.

- Review and approve the AML compliance program on a regular basis and ensure that it is aligned with the institution’s risk profile, business strategy, and regulatory obligations. The AML compliance program should include a risk assessment, policies and procedures, internal controls, training, monitoring, testing, reporting, and record-keeping.

- Provide adequate resources and training for the AML compliance staff and the relevant business units and ensure that they have the necessary tools and technologies to perform their tasks efficiently and effectively. The training should be tailored to the specific roles and responsibilities of the staff and should be updated regularly to reflect the changes in the AML risks and regulations.

- Evaluate and monitor the performance and effectiveness of the AML compliance program and take corrective actions when necessary (or at least once a year). This can be done by reviewing the reports and feedback from the AML compliance officer, the internal audit, the external audit, the regulators, and the law enforcement agencies, and by conducting periodic self-assessments and independent reviews. Senior management should also regularly (at least once a quarter) update the board of directors on the effectiveness of the AML program, key risk indicators, and any material developments related to AML compliance.

- Create and promote a culture of compliance and accountability within the institution and ensure that there are clear and consistent incentives and sanctions for the staff to comply with the AML policies and procedures. The incentives and sanctions should be proportionate to the level of risk and responsibility of the staff and should be applied fairly and transparently.

- Ensuring Compliance with Reporting and Recordkeeping requirements should be a priority for senior management. They should ensure that the FI complies with reporting requirements, including the filing of suspicious activity reports (SARs), and maintains appropriate records as per regulatory guidelines. Senior management should also establish effective communication channels with regulatory authorities, responding to inquiries, and cooperating with investigations.

By taking these actions, senior management can demonstrate their leadership and commitment to AML compliance and foster a positive and proactive attitude among the staff and the customers. This can help the institution to mitigate the AML risks, enhance the reputation, and achieve the business objectives.

Corporate and Personal Responsibility for AML Compliance

AML compliance has stopped being only a matter of corporate responsibility, but also a matter of personal accountability. Senior management, who play a vital role in ensuring AML compliance within their firms, may face individual liability if they fail to fulfill their AML obligations or if they are involved in or aware of any AML violations. Therefore, senior management should adopt the best practices in AML, and exercise due care and diligence in overseeing and managing the AML risks and challenges that they face.

How Actimize can help?

We have a strong group of AML consultants who can help board members and senior management drive compliance culture and navigate through the challenges by providing tailored training to the FI’s employees. To know more about our training and other advisory services, please go through our service catalog here or get in touch.